Search

Insights

Show Filters

Location

-

Australia & NZ

-

Canada

-

Europe

-

UK

-

USA

Category

-

Ad Categories

-

COVID-19

-

Digital Media

-

Market Trends

-

News & Events

-

Newspaper Ad Spend

-

NFL

-

OTT

-

Release Note

-

Television

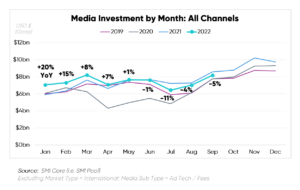

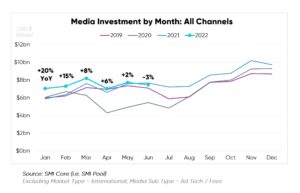

U.S. SMI Core Release Note – October 2022

November 17, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, representing up to 95% of all US national brand ad spending, to provide a complete monthly view of the SMI Pool market size, investment share and category performance. Core Data delivers detailed ad intelligence across all media types, including Television, OTT, Digital, Out of Home, Print, and Radio....

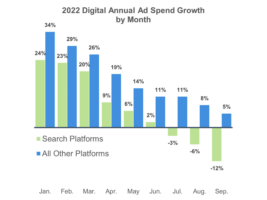

Retail Media is Here in a Big Way: Should Search be Worried?

November 4, 2022

By John Spiropoulos

Media is filled with evolutionary step-change transitions which permanently alter the marketplace. Each evolutionary event, seen in terms of advertiser outla...

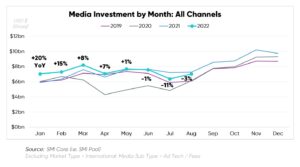

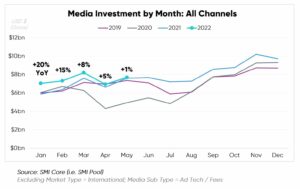

U.S. SMI Core Release Note – September 2022

October 20, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, repres...

Future of TV Advertising Canada 2022

October 9, 2022

In this session from the Future of TV Advertising Canada Forum, Darrick Li, Managing Director of Standard Media Index, looks at the driving factors to the ad market rebound in Canada.

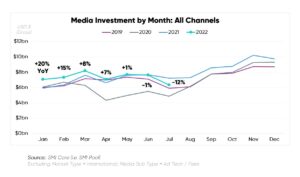

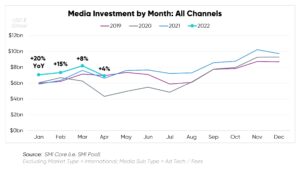

U.S. SMI Core Release Note – August 2022

September 26, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, repres...

U.S. SMI Core Release Note – July 2022

August 16, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, repres...

Recession Planning, Part 4: Brands, know your fundamentals and keep goals flexible

U.S. SMI Core Release Note – June 2022

July 19, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, repres...

Recession Planning, Part 3: Publishers, stay ahead of the changing mix accelerated by recessions

Recession Planning, Part 2: One thing to expect from a recession: restacking of the media mix

Recession Planning, Part 1: What a broad recession would mean for the ad industry

June 29, 2022

Part 1 in a 4-part series on recession planning for advertising

By John Spiropoulos

...

U.S. SMI Core Release Note – May 2022

June 17, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, representing up to 95% of all US na...

U.S. SMI Core Release Note - April 2022

May 24, 2022

SMI Core data captures the actual spend data from the SMI Pool partners of major holding companies and large independent agencies, repr...